Original Publication

Exploring the Cointegration Relation among Top Eight Asian Stock Markets

2020, January, Open Journal of Business and Management 08 (03), pp 1076-1088

KEYWORDS = Co-integration, Eigenvalue, Portfolio, Granger Causality

PUBLICATION, 6 AUTHORS :

- Muhammad Rizwanullah

- Lizhi Liang

- Xiuyuan Yu

- Jinan Zhou

- Muhammad Nasrullah

- Muhammad Uzair Ali

CCPR, ONLY YOU and CCPR

- Research Duplication = 2 seconds

- Research Improvement (100 World Wide Indexes, cover about 80 countries)= less than 1 minute

- Data: 8 representative index or stock for top 8 Asian countries

- Frequency/Period : Daily, 2000-2017

- Tests: Unit root (Augmented Dickey Fuller, Philip Perron), Co-integration (Johansen), Causality (Granger)

- Results: Causality test also shows the indication of short term relation

- Publication: 2020, publication-end of data > 2 years

Table 1: Data

Load Data from CCPR Server Database (Execution time = 0.1 second)

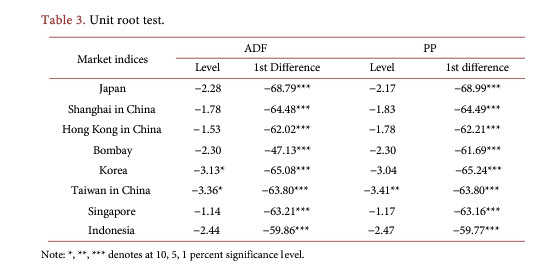

Table 3: Unit Root Tests

Original

By CCPR (Execution time = ADF+PP = 1 second)

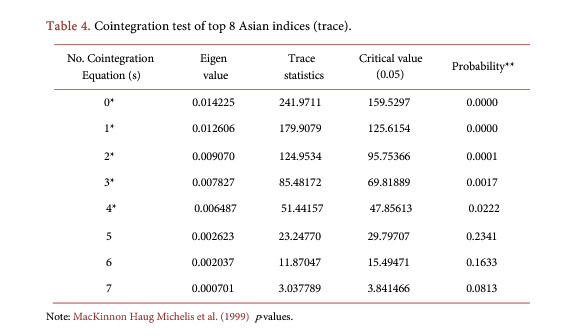

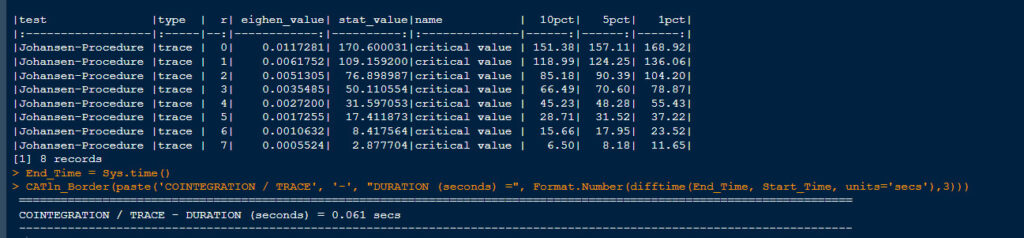

Table 4: Cointegration Tests (Trace)

Original

By CCPR (Execution time = JOHANSEN/TRACE = 0.1 second)

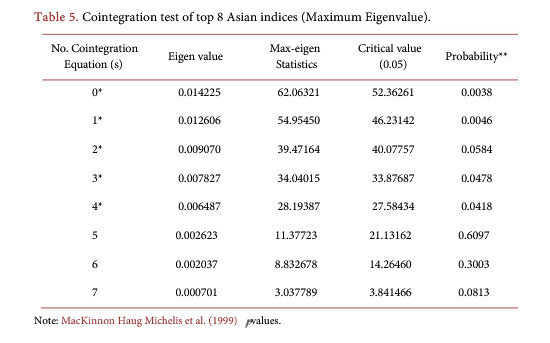

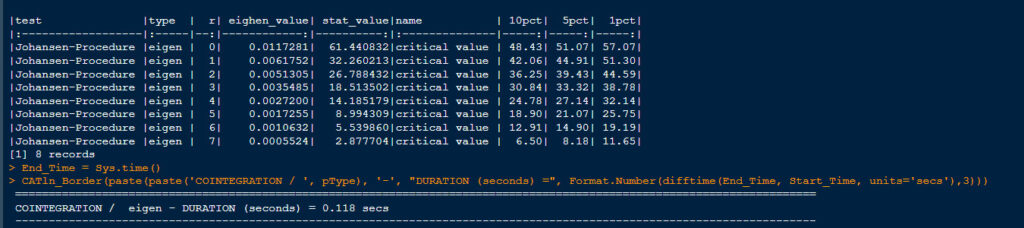

Table 5: Cointegration Tests (Maximum Eighenvalue)

Original

By CCPR (Execution time = JOHANSEN/EIGEN= 0.1 second)

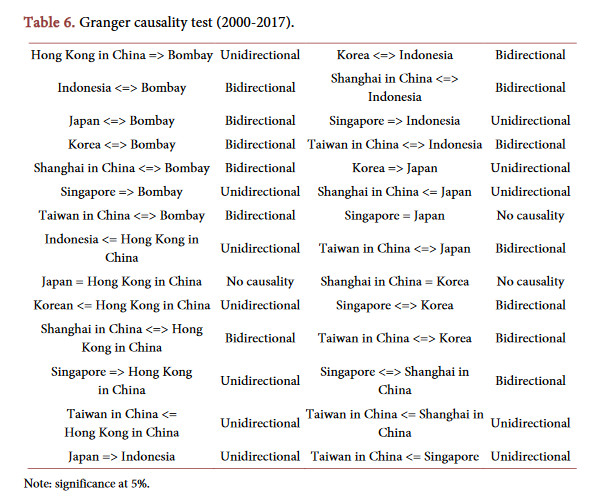

Table 6: Causality Tests (Granger)

Original